The 4% Rule and Retirement Income Planning

Dr. Doug Yang

Investment Adviser

What Is the 4% Rule?

Consider the following so-called retirement income problem:

"A man is retiring and has saved a lot of money for retirement. How much money should he withdraw each year from his savings, so that his money will confidently last 30 years"?

If withdrawing too much, the money may not last his lifetime. If withdrawing too little, his hard-earned money is not best utilized to enjoy life.

Published in Journal of Financial Planning, 1994, financial advisor William P. Bengen provided an answer: withdraw 4% of the savings in the first year of the retirement and adjust the withdrawals for inflation in future years. Then the chance of not running out of money in 30 years is about 90%. Mr. Bengen arrived at this conclusion after performing simulations using historical data on stock and bond returns over the 50-year period from 1926 to 1976, assuming a 50/50 portfolio (50% of the assets invested in stocks and 50% in bonds).

Here is how the 4% rule works. Suppose he has $2 million allocated to generate yearly retirement income. In the first year of retirement he withdraws 4% of that amount, or $80,000. In the second year of retirement, he adjusts his withdrawal amount for inflation. If the inflation rate is 2% in the previous year, he takes out $81,600 for the second year. He continues to take these yearly inflation-adjusted withdrawals over the course of his retirement for the rest of his life.

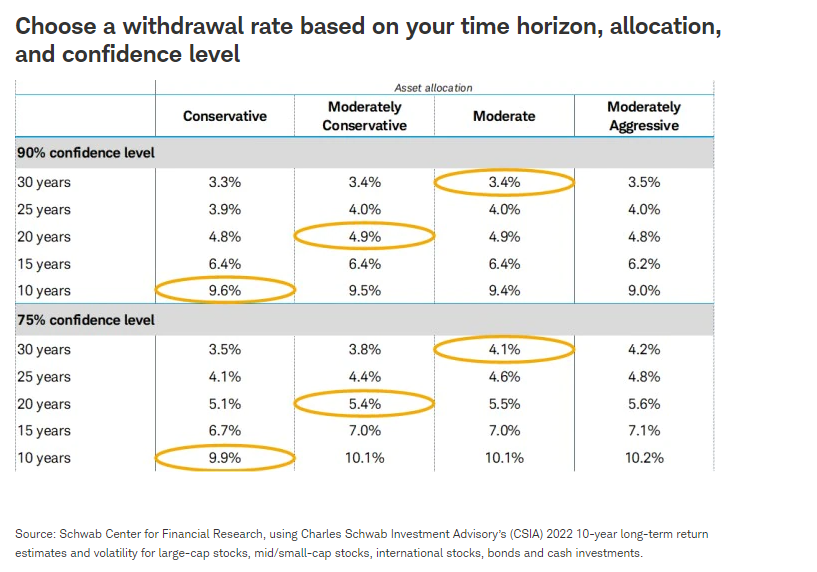

The 4% rule is a rule of thumb. It is meant to be used as a general guideline. Due to low interests in bonds, Morningstar lately did more simulations using recent stock and bond returns and suggested that a safe starting withdrawal rate be 3.3%, instead of 4%. This is consistent with Schwab's result for a conservative investor. Schwab further states that the initial safe (with 90% confidence level) withdrawal rate can be 3.4% for a moderate investor and 3.5% for an aggressive investor.

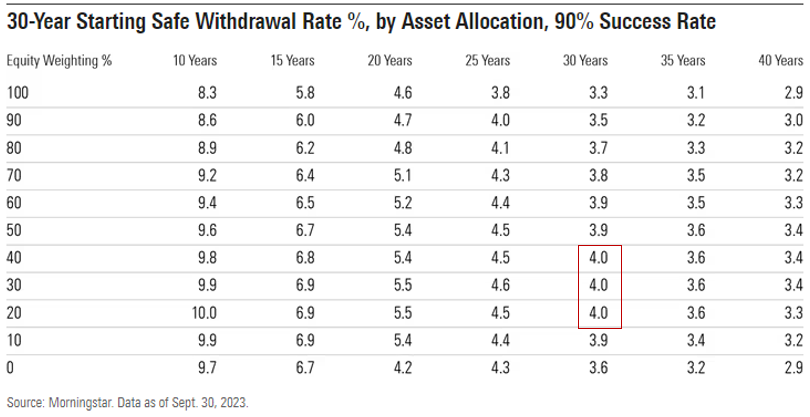

With the rising bond yields, as of September 2023, Morningstar improved the safe withdrawal rates to 4% for a diversified portfolio with 20% to 4o% stocks. Note that more stocks may not be better in the distribution phase.

"A man is retiring and has saved a lot of money for retirement. How much money should he withdraw each year from his savings, so that his money will confidently last 30 years"?

If withdrawing too much, the money may not last his lifetime. If withdrawing too little, his hard-earned money is not best utilized to enjoy life.

Published in Journal of Financial Planning, 1994, financial advisor William P. Bengen provided an answer: withdraw 4% of the savings in the first year of the retirement and adjust the withdrawals for inflation in future years. Then the chance of not running out of money in 30 years is about 90%. Mr. Bengen arrived at this conclusion after performing simulations using historical data on stock and bond returns over the 50-year period from 1926 to 1976, assuming a 50/50 portfolio (50% of the assets invested in stocks and 50% in bonds).

Here is how the 4% rule works. Suppose he has $2 million allocated to generate yearly retirement income. In the first year of retirement he withdraws 4% of that amount, or $80,000. In the second year of retirement, he adjusts his withdrawal amount for inflation. If the inflation rate is 2% in the previous year, he takes out $81,600 for the second year. He continues to take these yearly inflation-adjusted withdrawals over the course of his retirement for the rest of his life.

The 4% rule is a rule of thumb. It is meant to be used as a general guideline. Due to low interests in bonds, Morningstar lately did more simulations using recent stock and bond returns and suggested that a safe starting withdrawal rate be 3.3%, instead of 4%. This is consistent with Schwab's result for a conservative investor. Schwab further states that the initial safe (with 90% confidence level) withdrawal rate can be 3.4% for a moderate investor and 3.5% for an aggressive investor.

With the rising bond yields, as of September 2023, Morningstar improved the safe withdrawal rates to 4% for a diversified portfolio with 20% to 4o% stocks. Note that more stocks may not be better in the distribution phase.

The Sequence Risk

The sequence risk, also called the sequence-of-returns risk, is often associated with the 4% rule.

A retiree may have a successful retirement with one sequence of returns, but runs out of money with another sequence of returns,

although the average annual growth rates of the two sequences of returns are the same.

See the reference articles below for a better understanding.

The harsh reality of the 4% rule and the sequence risk is this. Two people retire in different years, but have saved the same amount of money for retirement, and both follow the 4% rule with exactly the same starting withdrawal rate. Due to the sequence risk, they could end up with one being successful but the other running out of money prematurely.

The harsh reality of the 4% rule and the sequence risk is this. Two people retire in different years, but have saved the same amount of money for retirement, and both follow the 4% rule with exactly the same starting withdrawal rate. Due to the sequence risk, they could end up with one being successful but the other running out of money prematurely.

Can We Do Better?

If an investor manages his money himself, the 4% rule is easy to use.

But it is not guaranteed to be successful in having the money last his lifetime.

He may still face the risk of running out of money prematurely.

As a retiree grows older, his portfolio would shift more towards bonds, while bond yield is historically low.

This would put more pressure on his retirement income and on maintaining the same purchasing power due to inflation.

The question is: can he reduce his sequence risk, improve his success rate, and get more income to spend each year

than what the 4% rule gives him?

The answer is yes, but with the help of a qualified professional.

We will be happy to help with your retirement income planning.

Some Articles from Reputable Sources

The following articles may help you understand what

the 4% rule is and what main issues it is aimed to resolve. It is critical to understand its pros and cons.

If not done correctly, your retirement could be ruined, or not as enjoyable as it should be. Seeking professional help early is recommended.

- What Is the 4% Rule?

- The 4% rule is being debated — again — but here’s what you should do

- The 4% Rule Faces New Problems Today

- Beyond the 4% Rule: How Much Can You Spend in Retirement?

- Sequence Risk During Retirement

- How Would Another Drop in the Market Affect Your Retirement Assets?

- Sequence of Returns Risk

This page is for general information only and is not intended to provide specific advice

for any individual.